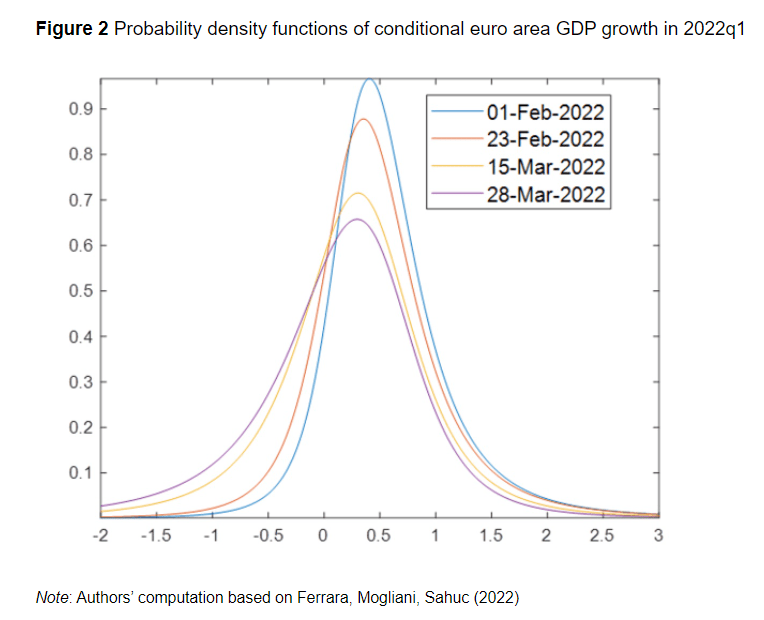

Following the Russian invasion of Ukraine on 24 February 2022, financial stress indicators suddenly increased. Using this high-frequency daily information conveyed by financial markets, this column presents a newly developed mixed-frequency quantile regression model in order to quantify macro risks in the euro area for the first quarter of 2022. The authors show that macro downside risks perceived by financial markets in the euro area are about three times higher than those for the US economy.

https://voxeu.org/article/war-ukraine-and-high-frequency-macroeconomic-risk-measures